Last week, the Triangle Mortgage Lenders Association (TMLA) hosted a luncheon for the Durham Regional Association of Realtors (DRAR), complete with an insightful presentation from Devon Hawkins, Professor of Economics at Elon University, entitled:

“No-Bull Rates in 2026: A Reset, Recalibration, and What it Means for Real Estate Professionals”.

Hawkins clearly laid out what’s happened over the past 5 years to get our economy to where it is now, and how that will shape mortgage rates over the next several years.

The key takeaways? The housing market is not broken; our country’s economy is recalibrating, 3% mortgage rates were historically abnormal. And the next phase of the market will look different. Not worse, but different.

Hawkins brought it all back to the real estate professional. It’s our job to inform and set real expectations for buyers, sellers, and borrowers in this “new normal” we are in. And feel comfortable participating in the economy by buying, selling, or refinancing a home.

And rate projections for 2026? She went over that too. Don’t worry, we’ll go over it here.

So let’s get into it, shall we?

The Big Reset: 3% Was Never Normal

Oh, what a time it was to be alive with 3% mortgage rates. Amongst a pandemic, there was still a slight pep in people’s steps, knowing they just put a down payment on a dream home they never thought was even possible.

Current homebuyers and sellers want to know when we can expect that Saturn return again, and the answer is, probably not in our lifetimes. Once you come to understand exactly why rates were so low, it’s easier to understand how they were such a rarity.

During the COVIID-19 Pandemic, economic activity came to a standstill. No one was going to restaurants or concerts or supporting local businesses, which led to a plunge in economic activity.

To stimulate some economic activity in place of all that, rates were lowered dramatically, in hopes that people would seize the opportunity, and it worked.

An incredible housing boom occurred from 2020 to 2022 because of it, and now we have a mixed bag of people who:

- Seized that opportunity and now live in their dream home

- Took the plunge to their next home, but don’t feel settled in it and are waiting for 3% rates to move again, because how could you let that go? (You can let it go, and you should if it’s the right fit, keep reading)

- Let that opportunity pass by and are waiting for it to come back around (newsflash, it’s not coming)

Hawkins’ advice to Durham Realtors facing these real conversations with potential clients is to explain the timeline, clarify why 3% happened, why it’s not happening again, and how to navigate the market moving forward. For the past year or so, the market has been recalibrating to a more historically consistent environment.

Why Mortgage Rates Drive Everything

So, we’ve covered how the 3% mortgage rate came to be and why it’s not coming back any time soon. Now let’s talk about why mortgage rates drive behavior and what that means for both our clients and our business strategy.

A. Housing Is Highly Elastic

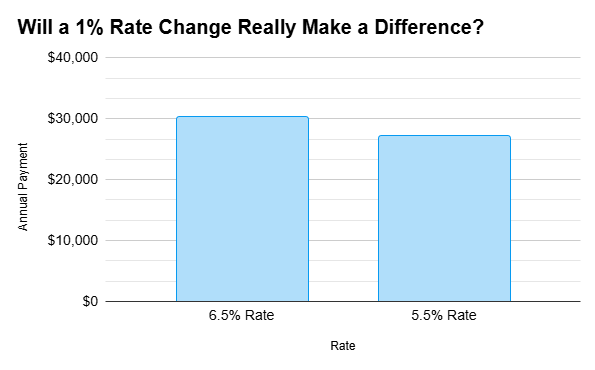

First, housing is highly elastic. There’s a give in any transaction between the sale price and the list price. And when a homeowner is looking at their monthly mortgage payment, they’re thinking about just that- monthly payments. Not the full price they’re spending on a home. And where are the monthly payment amounts derived from? Your mortgage rate. To paint this picture, here is an example:

Calculation is based on $400,000 home with a 30-year fixed mortgage.

- At 6.5%: ~ $2,528 /month

- At 5.5%: ~ $2,271/ month

That’s ~$250 monthly or $3K difference annually

Source: Presentation by Devon Hawkins, Professor of Economics, Elon University (TMLA/DRAR Luncheon). Graphic recreated for educational purposes.

So while 3% rates are done and dusted, there is still an opportunity for smaller monthly payments in our current market. Even just a 1% rate difference can save a homeowner thousands annually.

B. Why Transaction Volume Matters More Than Price

Again, take the pandemic for example. During that time, list prices were astronomical, and homes were still being sold over-asking price in crazy bidding wars.

Why? Because clients wanted to seize the day with those beautifully low rates.

So, moving forward, Hawkins real estate professionals should not stress over prices, but rather focus on their volume and on helping their clients understand the current market.

TAG Tip: In a market where pricing requires more precision, a pre-listing appraisal can ground expectations before a property ever hits the MLS. It gives sellers clarity and gives you stronger footing in listing conversations. And if you just need to talk through a tricky property, the TAG team is always happy to be a sounding board.

How Mortgage Rates Are Determined

A lot of people (me included, before this presentation) think mortgage rates move because “the Fed said something”.

Well, that’s not really how it works.

Rates move because of bigger forces at play. And once you understand those forces, the headlines and current rates feel a lot less dramatic.

Let’s break it down simply.

A. Inflation is the Primary Driver

If you remember one thing, let it be this:

When inflation rises, mortgage rates usually rise too.

Here’s why.

Investors who buy bonds (which ultimately fund mortgages) want to be repaid with money that retains its value. If inflation is high, their money loses purchasing power. So they demand higher returns.

Higher inflation → Higher bond yields → Higher mortgage rates.

Right now, inflation is cooling. That’s good!

But we’re not yet fully back to the Fed’s 2% target.

Which means rates don’t collapse overnight. They ease slowly.

B. The 10 Year Treasury is the Anchor

If you want to know where mortgage rates are heading, Hawkins advises real estate professionals to watch the 10-Year Treasury yield.

Mortgage rates typically run about 1.5%–2.5% above the 10-Year Treasury.

So when the 10-Year moves, mortgage rates usually follow.

It’s not exact. But it’s close enough that professionals should be paying attention.

If you’re a Realtor or lender, this is a better indicator than waiting for the evening news to mention the Fed.

C. The Federal Reserve Has Indirect Influence

The Fed controls short-term interest rates, not mortgage rates directly.

Mortgage rates are long-term rates. They move based on what investors expect inflation and growth to look like over the next 10 years.

That’s why sometimes:

- The Fed announces a rate cut

- And mortgage rates go up

Why?

Because investors already expected that cut. They had already adjusted the rates in advance.

Or…

Investors don’t think inflation is fully under control yet, so they’re not comfortable lowering long-term rates.

D. Labor and Economic Growth

Strong economic data can actually push rates higher.

If job growth is hot and wages are rising fast, inflation pressure can return. Investors then demand higher yields. Rates rise.

On the flip side, if the labor market cools and growth moderates, it supports stabilization.

Not collapse. Stabilization.

That’s the phase we’re moving toward.

E. MBS & Credit Spends

Here’s one more piece most people never hear about.

When you get a mortgage, that loan doesn’t just sit at your local bank. It gets bundled together with thousands of other mortgages and sold to investors.

Investors decide how attractive those mortgage investments are.

If investors feel confident about the economy, they’re comfortable earning a little less. That helps keep mortgage rates lower. If investors feel nervous about inflation, the economy, or risk in general, they want a bigger return. That pushes mortgage rates higher.

And here’s the important part:

Mortgage rates can move even if the 10-Year Treasury doesn’t move much.

That’s why sometimes rates feel unpredictable. There’s more happening behind the scenes than just one headline number.

How We Got Here: The Strategic Timeline

2020–2021 Pandemic Liquidity → Aggressive rate cuts + massive stimulus → Mortgage rates near 3% → Historic housing surge

2022 Inflation Surge → CPI spikes → Bond markets reprice risk → Rates begin climbing

2022–2023 Rapid Fed Tightening → Fastest rate hikes in decades → Mortgage rates above 7% → Affordability shock → Volume contracts

2023–2024 Lock-In Effect → Majority of homeowners under 4% → Resale inventory freezes → Builders gain share

2024–2026 Stabilization Phase → Inflation cooling → Bond markets steady → Gradual rate drift downward → Market recalibrating

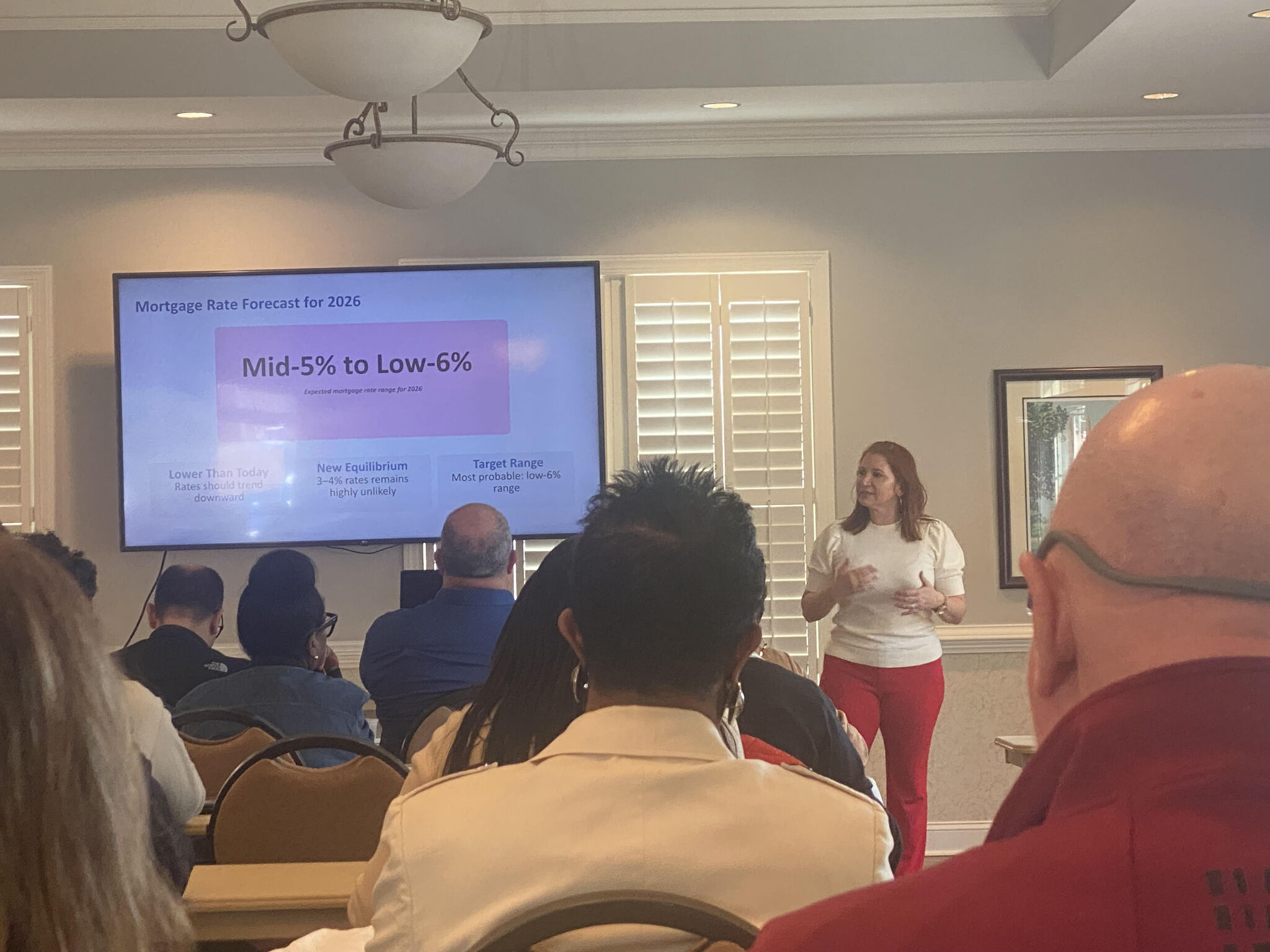

2026 Mortgage Rate Outlook

The number one question for everyone in real estate is how the rate numbers will play out this year. With Devon Hawkins’ experience in economics and intimate knowledge of the North Carolina housing landscape, she predicts mortgage rates will range from the mid-5 % to the low-6 %.

Will there be a drastic cut to 3-4%? Probably not without severe recession, said Hawkins.

TAG Tip: As volume gradually returns, consistency and speed matter. TAG is established with over 200 AMCs across North Carolina and delivers residential reports within 3–5 days of inspection. In a competitive, purchase-driven market, dependable turnaround times make a measurable difference.

The Triangle & North Carolina Context

No two markets move the same way.

And when you zoom in on North Carolina, especially the Triangle, the foundation here looks very different than much of the national narrative.

For more than a decade, North Carolina has seen steady in-migration. People continue moving here for opportunity, career growth, and quality of life.

In just the last five years, the Triangle has welcomed major long-term investments, including:

These are high-wage, long-term job creators. When companies make investments at that scale, they are planning decades ahead.

And when jobs grow, population follows.

More households create sustained housing demand. That underlying demand remains, even if transaction volume has slowed over the past two years.

Inventory remains tight largely because many homeowners are sitting on historically low mortgage rates and choosing not to move. That dynamic has limited supply and slowed turnover.

From a fundamentals standpoint, the Triangle continues to be supported by job and population growth, as well as long-term corporate investment. The demand drivers are still in place.

That’s why Hawkins emphasizes the importance of Realtors and lenders educating their clients and helping them move forward with realistic expectations, rather than waiting on conditions that are unlikely to return. Confidence builds when buyers and sellers understand the landscape and make informed decisions.

As stability strengthens, economic activity tends to strengthen alongside it.

Final Takeaways

- The past few years have felt intense, but what we’re experiencing is a reset. Markets move in cycles, and this one is working its way back toward longer-term norms.

- The next housing expansion doesn’t begin when rates return to 3%. It begins when rates stabilize. Predictability builds confidence, and confidence drives participation.

- Housing is elastic. Buyers respond to direction more than perfection. Even modest rate improvements can shift monthly payments enough to bring people back into the market.

The Realtors and Lenders who stay active during this reset phase, who educate, set realistic expectations, and continue building relationships, position themselves well for the recovery that follows.

This recalibration season isn’t about waiting for perfect conditions. It’s about recognizing where we are and helping clients make informed decisions within it.

Connect with Rachel Mann Slonaker on LinkedIn:

Thanks for reading! We love sharing insights from the TAG team, and we’re always looking to connect with others who are passionate about real estate, marketing, and community.

Have thoughts to share or want to collaborate on a future post? Let’s talk!